The rebound in oil prices: OPEC “fine tuning” in question

In late September 2016, the Organization of Petroleum Exporting Countries’ (OPEC) agreement to reduce crude supply was particularly telling. Combined with the improvement of some fundamentals, the agreement in principle created the conditions for a rebound in oil prices. Speculative dynamics to benefit from this upturn are however at work in a market context where production overcapacity remains present. The price recovery remains fragile and a paradigm shift will occur only if OPEC manages to give the agreement an operational scope in the medium term. In addition to (geo)constraints and the strong policies that it implies, it is clear that the task will be a challenge. OPEC should indeed deal with the reality of global supply and engage in a policy of "fine tuning" to keep prices within a fluctuation band for improving the financial situation of its members, without however boosting the production (too much) of other producing countries.

The agreement to reduce oil production by the Organization of Petroleum Exporting Countries (OPEC) members, obtained at the end of September 2016, definitely surprised market observers. In fact, no one had expected that OPEC would agree to bring its crude supply between 32.5 and 33 mb / d (million barrels per day) while it had risen to 33.75 mb / d the previous month. If the agreement is formalized at the conference on November 30 2016, it seems that anyone who thought that the cartel organization was a cartel only in name will have been mistaken. The agreement was all the more surprising as it is the first in eight years and also because Saudi Arabia, the world's largest crude producer and primary OPEC member, and Russia, together expressed their willingness to cooperate to limit their production. A few months earlier, the Saudi kingdom had seemed to accept levels of sustained low prices and had consecutively engaged in an economic diversification strategy. The natural consequence of this apparent change of tone: the price of Brent and West Texas Intermediate, the two main global crude references, recovered strongly, reaching their highest level in a year, to over USD 50 / bbl at the beginning of October.

This increase, admittedly, is not only related to the Algiers agreement, although it has had an undeniable impact on market psychology: in recent weeks, surprised operators also welcomed an improvement in certain fundamentals, foremost among them a decline in US commercial reserves of crude. It is important to recognize that these fundamentals remain fragile and that the agreement leaves open a number of important issues, to the point where today it seems risky to bet on a significant increase in prices. Despite a reduction in the supply of some countries in recent months, oil production remains at record levels. A year of rebounding oil prices, 2016 will therefore also be one of high volatility, like many other commodities, as uncertainty about the reality of this agreement will continue.

Toward a market correction?

While the considerable drop in prices observed from the second half of 2014 was due to supply and demand factors, it must be recognized that the autumn 2016 rebound is primarily related to a reduction in supply or, at least, to favorable prospects in this area. The agreement to reduce production by OPEC members, ranging between 32.5 and 33 million bbl / d, could well be perceived as positive by market operators. The statement by Vladimir Putin, at the World Energy Congress on October 10, 2016, evoking a possible cooperation by Russia with OPEC to stabilize or restrict oil supply could only strengthen this bullish momentum. Thus, between September 28, 2016, date of the Agreement, and October 12, the Brent price rose over 12% to almost 52 USD, regaining its June 2016 level. The surprise was even greater as this followed a succession of decisions that favored increased production by 14 member countries: the refusal to reduce supply following the Vienna meeting on November 27, 2014, the abandonment of production targets early in December 2015, and the failure of the Doha meeting in April 2016, whose aim was precisely to agree on a new production objective to support prices.

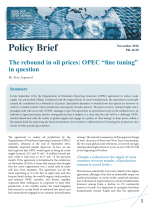

Clearly, the recovery in oil prices is not solely due to OPEC’s decision. Fundamental factors support this dynamic, and partly US-related ones. US oil production has indeed increased to 269 million barrels in July 2016 compared to nearly 292 million a year earlier (Figure 1).

Figure 1: Monthly U.S. crude production (In millions of bbl)

Source: US Energy Information Agency

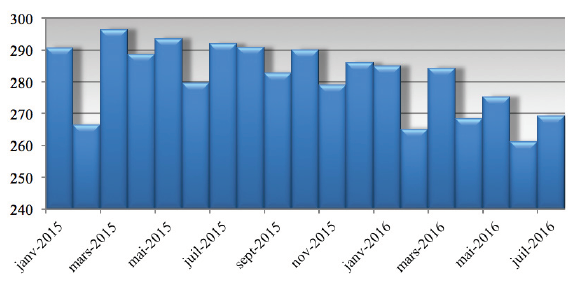

This decline is also seen in terms of the number of oil wells in operation (Figure 2). Although the productivity of wells should be taken into account to conclude about the level of production, the decline in US activity is indeed considerable: from 787 wells in late October 2015 to just over 550 a year later, which is a drop of nearly 30%. At less than 60 USD / bbl, a large share of shale oil reserves has become uneconomic.

Figure 2: Number of wells in the U.S. (by type)

Directional, Horizontal, Vertical

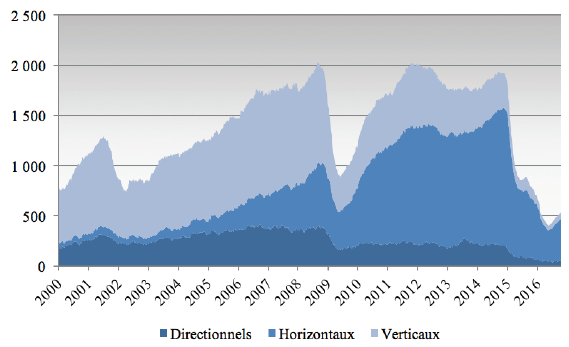

The substantial decline in commercial reserves of US crude is also one of the main factors behind this rebound. They went below 500 million barrels September 30, 2016, down sharply (-8%) since the historical high reached on April 29 of the same year (Figure 3). The same holds true for the reserves in OECD countries estimated at 3.092 billion barrels, according to statistics from the International Energy Agency (IEA). In other words, if the market remains in an over-capacity situation, the extent of the imbalance seems to be minimized, which the markets can only see positively. Regarding the demand for crude, nothing very positive however: it has certainly progressed in 2015 but this improvement is explained quite extensively by a "price effect" linked to the ability to buy cheap energy rather than a genuine improvement in global growth prospects (Arezki and Matsumoto, 2016).

Figure 3: Commercial crude reserves in the U.S. (In millions of bbl)

Source: US Energy Information Agency

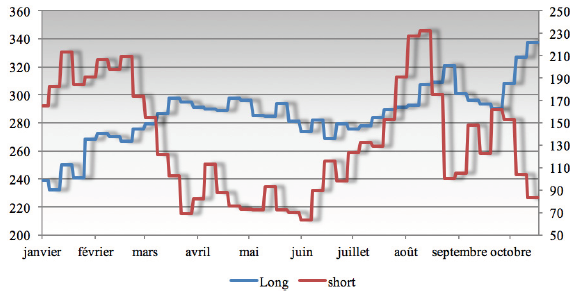

Beyond the evolution of these variables, it should be noted that speculative dynamics are also at work in the swap oil markets for Brent or WTI. Thus, according to data from the Commodity Futures Trading Commission (CFTC), in October, investment funds positioned on the New York Mercantile Exchange (Nymex) significantly increased their long positions on light crude, which is a sign of an anticipated increase in prices, and of the relative fragility of the rebound observed (Figure 4). For proof, the market prices have since significantly weakened.

Figure 4: Money manager positions (open-interest)

Source: Datastream

In the absence of a real return of global economic growth, the recovery of crude oil prices is thus based on the announcement of a hypothetical contraction in supply and on the "psychology" of the markets, which, beyond the surprise effect, continue to question not only the ability of OPEC producers to give this agreement in principle a strong operational reality during the meeting in Vienna on November 30, but also on its actual length if were to be endorsed. It is indeed clear: in terms of the game theory, cooperative equilibrium is certainly a non-preferential optimum ensuring the "best solution" for all participants, but it often acts as a mirage because the incentive to "cheat" remains strong. In any case, the price recovery should only be relative as the supply of oil has increased over the past several months: at 97.2 mb / d in September 2016, the world has never produced as much oil. Operators are unmistaken because the market structure of the Nymex and the International Continental Exchange (ICE) show an overall increase in contangos, a sign that the market will remain well-supplied. Regardless, actually, as it is recognized that OPEC’s ambition has probably never been to trigger a significant rise in crude prices through this agreement, but instead to keep them within a fluctuation band so member countries regain fiscal margins without nevertheless stimulating the production of non-members. To be convinced, perhaps it is necessary to cite Wirl (2008), who highlights, based on a theoretical model, that Saudi Arabia’s interest in promoting price volatility, rather than engaging in a strategy to maintain a certain level of oil prices. Toward a fine-tuning of crude supply? It is actually in view of this objective that the success -or the failure- of OPEC will be apprehended. Suffice to say that, from this perspective, there are many uncertainties.

Major questions

First, the OPEC agreement does not specify the terms of this supply reduction. Thus, it is unclear when the agreement could enter into force, on which this effort would concretely be based on, and what countries, aside from Nigeria and Libya, would be exempt. Iran has reiterated its willingness to achieve a production volume of 4 Mb / d (compared to 3.89 today) in the coming weeks, while Nigeria, deprived of foreign exchange earnings, aspires to increase its output of 400,000 Mb / d to 2.2 Mb / d. If market observers can expect Saudi Arabia to return to the role of "swing producer" it has historically played in the organization, any news highlighting the difficulties in making this agreement a reality will have a negative effect on prices. On the Nymex, the price of futures contracts dropped on Monday, October 24 after Jabbar Ali al-Louaïbi, Iraqi Minister of Oil, said that his country, the second largest producer of the organization, should legitimately be exempted from the agreement because of the conflict in which it is engaged. As evidenced by the recent statements by the Venezuelan President Nicolas Maduro, the idea that some non-OPEC producing countries - in addition to Russia- join this attempt to control supply is however possible, a priori.

A key point of the ongoing negotiations to reach an operational agreement: the estimated OPEC production volumes also remain challenged by some members including Iran, Iraq and Venezuela. Iraqi authorities estimate that their crude supply stood at 4.7 mb / d, while OPEC estimated it at 4.2 mb / d. Obviously, if Iraq were to reconsider the principle of freezing its production at the current level, this difference of opinion would weigh heavily in the negotiations. The question also concerns the behavior of other producers if prices were to exceed USD 60 / bbl, notably American and Chinese producers. Over the past weeks, the number of actively drilled wells in the US rose again from the low point in May 2016. Between September 2 and October 21, it jumped over 11% (553 compared to 497), returning to the February 2016 level. No doubt this figure will continue to grow if prices recover. The same holds true for China, whose oil production is widely expected to increase if crude prices were to reach such a level. In this respect, the forecasters were largely mistaken when crude prices began their fall in the second half of 2014. The reason: a difficulty in assessing the rapid technological developments that had benefited unconventional oil producers, which gave them the ability to, within a few months, attain a "break-even" point much lower than anticipated.

Moreover, if the supply behavior of the major exporters obviously has a decisive influence on the future level of crude prices, many other variables must be considered, and there is again a matter of speculation. Among these considerations is the evolution of the US dollar against the currencies of producing countries. Besides the well known effect of an increased energy bill for importing countries when the dollar appreciates, as it is the crude trading currency, it should be noted that producer countries that do not have a fixed exchange rate plan with the US regain economic leeway when their currency depreciates vis-à-vis the US currency. This can then allow them to maintain high production levels even as international oil prices are low. It is therefore understandable why the US Federal Reserve is currently the focus of attention.

In looking beyond short-term concerns in order to understand the market in its structural dimension, the current OPEC strategy naturally raises the question concerning the characterization of this group’s behavior: does OPEC behave has as a cartel or, more prosaically, as an oligopoly in which one or more of its members - first and foremost Saudi Arabia- play a key role? To this question, the numerous empirical studies that have been conducted over the past decades provide measured responses. The idea that the organization, as a whole, produces in a coordinated manner in order to influence the price, over a long period does not seem confirmable. Among the most recent studies, Kisswani (2016) shows that during the period from 1994 to 2014, a co-integration relationship between the production of each OPEC member and the total production of the organization does not exist, leading the author to conclude an absence of coordinated production levels and thus of cartelization. Beyond the somewhat rhetorical question regarding the qualifying OPEC as a cartel and a sometimes vain attempt to model its behavior, a question arises: Does the organization have a decisive influence on crude prices and, where appropriate, under what conditions? Bremond et al. (2012), reflect this approach by demonstrating that OPEC has predominantly acted as a "price-taker" for the period between January 1973 and July 2009, thus confirming the organization’s inability to guide the market. Brunetti et al. (2013) question the scope of OPEC statements on what it considers the "real" price of crude and similarly conclude the absence of the organization’s veritable market power. Kisswani’s (2016) analysis also shows that OPEC does not seem able to influence the price level through its supply behavior and in reality, world prices instead influence the OPEC production level, and not the inverse. The study by Loutia et al. (2016) on the impact of announcements made during official or special meetings on the dynamics of Brent and WTI prices (March 1991-February 2015), however, offers different perspectives. The authors especially emphasize that, depending on the nature of the announcement (maintenance of quotas, reduction, increase) prices react in a differentiated way, in both their level and volatility, regardless of the obvious supply and demand factors: an announcement to maintain or reduce oil supplies has thus an impact on market dynamics, while an announcement to increase quotas does not result in significant abnormal yields, which the latest developments in the oil markets have once again shown.

Whatever the scope of the empirical work, we must recognize that, economically, the implementation of an OPEC production cut agreement would resemble, at best, a Pyrrhus victory for Saudi Arabia, as the kingdom has suffered from falling prices. Politically, however, a potential success by this country would be pessimistic about the ability of the group to achieve it in the short term. If the agreement in principle has surprised many observers, perhaps the same will be said for the meeting in late November. Otherwise, oil prices are expected to experience a significant decline.